Few Signs Of Slowdown In AV Sector, At Least For Now, Despite Wobbling Global Economy: AVIXA

October 20, 2022 by Dave Haynes

The overall economy in North America and globally looks wobbly, but so far there are not a lot of signs of slowdown in the AV sector, based on the latest numbers in AVIXA’s monthly Pro AV Business Index.

Pro AV, says AVIXA’s research team, continues to grow quickly, even as the overall economy wavers. The comments (from industry people) make it clear that returning to in-person remains a driver of spending, whether for live events, corporate office space, hospitality, or others. The slower growth observed in June and July seemed to suggest this tailwind was blowing itself out, but the additional data shows that is untrue. On the negative side, workforce difficulties and especially supply chains stood out as the biggest ongoing business challenges.

A new factor was mentioned by a few commenters this month: exchange rates. For years, exchange rates among major currencies have been stable enough that their evolutions—even if significant over time—never stood out. That has changed. This year, major currencies have shifted dramatically, with a strengthening dollar the biggest trend. Higher interest rates instituted by the U.S. Federal Reserve Board make dollar-dominated bonds a newly attractive saving vehicle, creating demand for USD to purchase these assets. So far this year, the dollar has strengthened roughly 15% against the Euro, 12% against the Chinese Yuan, 26% against the Japanese Yen, and 19% against the British Pound. These shifts substantially affect equipment costs. For the U.S., it makes foreign-produced products cheaper. In Japan, where the Yen has weakened so substantially, foreign-produced products are more expensive. In China and the EU, U.S. products are more expensive, while Japanese ones are cheaper.

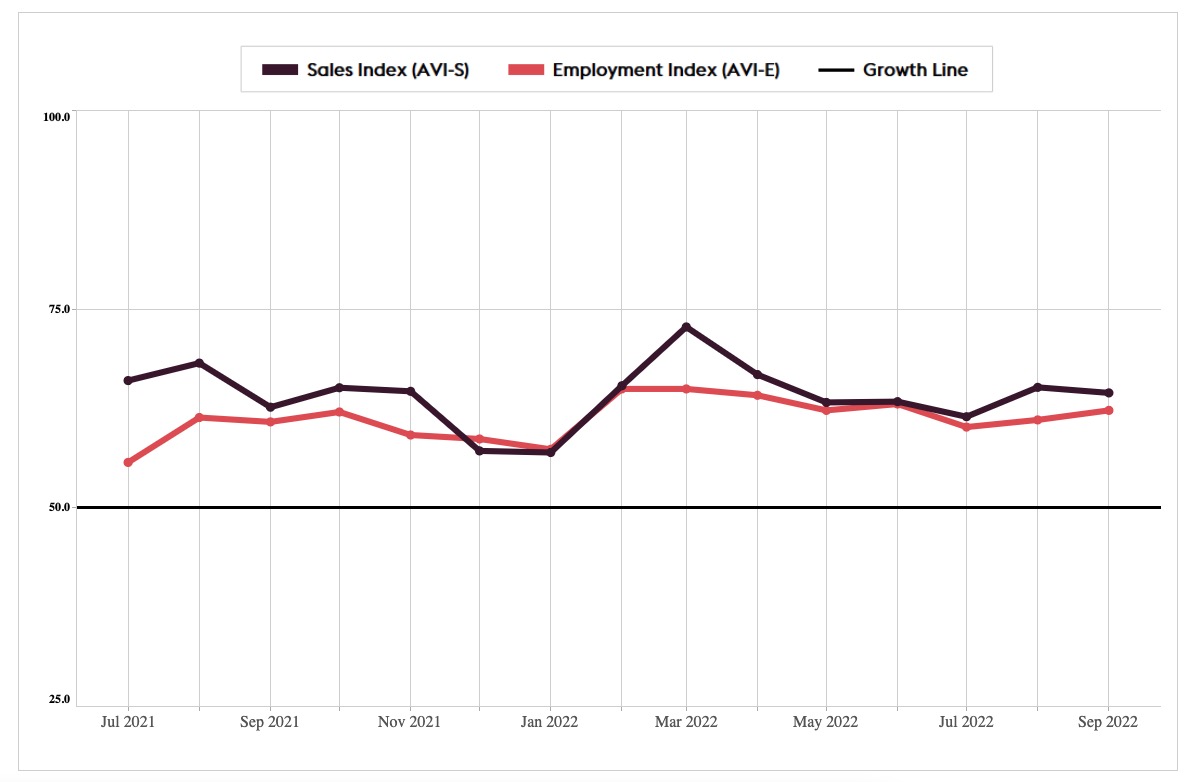

Pro AV hiring improved again in September, as the AV Employment Index (AVI-E) accelerated from 61.0 to 62.2. This comes amidst a backdrop of serious difficulty that centers on hiring, as revealed in our just-released Q3 META report. These high numbers in the AVI-E indicate continued and perhaps marginally worsening conditions for retention. In the wider economy, there are signs of deceleration amidst a still-hot market. Job openings in the U.S. dropped just over 1 million in August (the most recent release), though the level remains historically high—especially when compared to the number of available workers. The U.S. economy added 263,000 jobs in September, which is the lowest in a year but would have been high at any point in the decade leading up to the pandemic. To reiterate, the labor market is shifting, but demand for workers continues to substantially outstrip supply.

September marked a major move towards parity of growth in our International Outlook. After the Rest of the World outpaced North America by 3.5 points in our initial reading for August, September now shows North America a slim 0.3 points ahead of the Rest of the World. Last month we highlighted weakness in China and Europe, noting how this made the observed growth gap surprising. Perhaps the shift in these numbers reflects the frailty in those areas—though we stress that pro AV is growing strongly in all areas.

Explainer for that chart at top …

An index of 50 indicates firms saw no increase or decline in business activity; more than 50 indicates an increase, while less than 50 indicates a decrease.

Leave a comment