“Excessively High Inventory” In Flat Panel Display Value Chain: DSCC

June 14, 2022 by Dave Haynes

The display market research firm Display Supply Chain Consulting, also known as DSCC, has a post up on its site going into granular detail about the current glut of flat panel displays in the U.S. system, and the ramifications of that.

The numbers are about consumer TVs, but more broadly reference “excessively high inventory throughout the flat panel display value chain” and how that will force lowered prices and margins, and trigger production slowdowns for the second half of the year.

“Throughout the display value chain,” writes DSCC’s Bob O’Brien, “the surge in demand generated during the pandemic’s early days, combined with shortages and transportation problems, set in motion a path toward building a mountain of inventory. Now that the pandemic demand peak has passed, that big mountain needs to be consumed before a normal supply/demand balance can be restored.

A profit warning from US retailer Target on Tuesday, June 7th led to a sharp selloff in US retailer stocks and highlighted this issue among US retailers. Target CEO told the Wall Street Journal that Target was “chasing hard in 2021 to get more of the inventory that our guest was looking for.” In order to bring inventory under control, Target plans a summer of heavy discounts, “especially in categories that Target is carrying too much of, such as kitchen appliances, TVs and outdoor furniture,” per the WSJ. Target lowered its guidance for operating margin for 2022 in anticipation of discounting actions that will reduce margins.

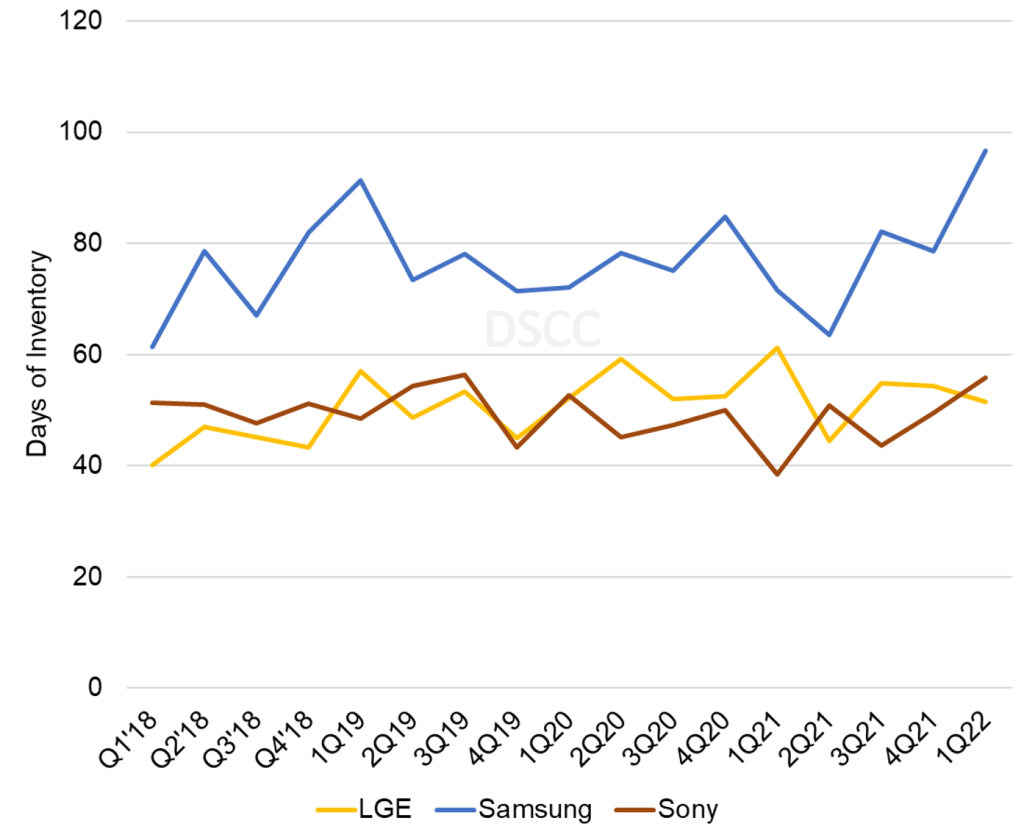

Among US retailers, Target could be considered a second-tier vendor in the electronics space. While Target does not disclose its revenues for specific product segments like electronics, an analysis of the company’s typical floor space suggests that electronics form only about 2-3% of the company’s revenue, which in 2021 was $106B. That means the company has only about a 1% share of US consumer hardware. A look at the larger players in the industry, though, demonstrates that the problem of excess inventory is not limited to Target, but is industry wide.

O’Brien qualifies his observations by noting they are backward-looking.

Most of the inventory data dates to the end of March; the retailer data dates to the end of April. Based on DSCC’s estimates of utilization rates at panel makers, the situation has not improved during Q2. Panel makers sustained high rates of utilization in April and May, while end market demand has continued to be weak.

So, with two weeks of excess inventory at retailers and another two weeks at panel makers, the industry has four weeks of excess inventory, or perhaps more than that at the end of Q2. Many have speculated that companies will want to carry more inventory post-pandemic to address the problems of supply chain uncertainty. This is likely to be the case, but it is unclear how much more inventory they will want to carry. On the other hand, if companies believe that a recession is imminent, they will try to conserve cash, and will therefore push to keep inventory to a minimum.

If the display industry needs to cut two weeks of inventory from the value chain during the second half of 2022, this will require a sharp slowdown of utilization in the industry. It means the industry needs an equivalent of 24 weeks of production for the 26 weeks of demand, that’s a reduction of 8% in overall utilization. If the industry needs to cut four weeks, then double the impact to 16%. Although we can’t be certain about the exact amount of the correction nor about the exact timing, it appears clear that the industry is headed for a slowdown in the second half of 2022.

You have to register to get full posts from DSCC, but there’s no cost.

Leave a comment