Pandemic Was, Weirdly, Best Of Times For Display Industry, While Recovery Is Worst Of Times: DSCC

May 17, 2022 by Dave Haynes

The digital display industry finds itself in this weird circumstance, says supply chain analyst Ross Young, in which the 2020-2021 pandemic period was actually pretty good, and now, as the recovery ramps up and inflation is rising, prices are down and the outlook is shaky.

Display Supply Chain Consulting’s Young made that observation in a keynote last week at the Society for Information Display’s Display Week conference In Silicon Valley. DSCC always does an excellent business conference at the event, which attracts the engineering and business side of the display industry.

“2020 and 2021 were the best of times,” Young writes in a summary of his talk. “Everything went right for the display industry – higher units, higher prices, tight supply, lower costs, rich product mix, higher margins, etc.”

“2022 is the worst of times, everything is going wrong for the display industry – lower units, lower prices, loosening supply, higher costs, lower margins. Prices expected to fall to cash costs in some cases. The display industry will remain cyclical. Over investment over the last two years is contributing to the current sharp price reductions. There will be a large drop in capex next year and may see additional capacity come offline. Furthermore, over-investment in IT markets is a concern with LCD and OLED suppliers all targeting the same markets with significant new capacity.”

The summary is on the DSCC site, but you will need to register to get at it. Here’s more from the summary:

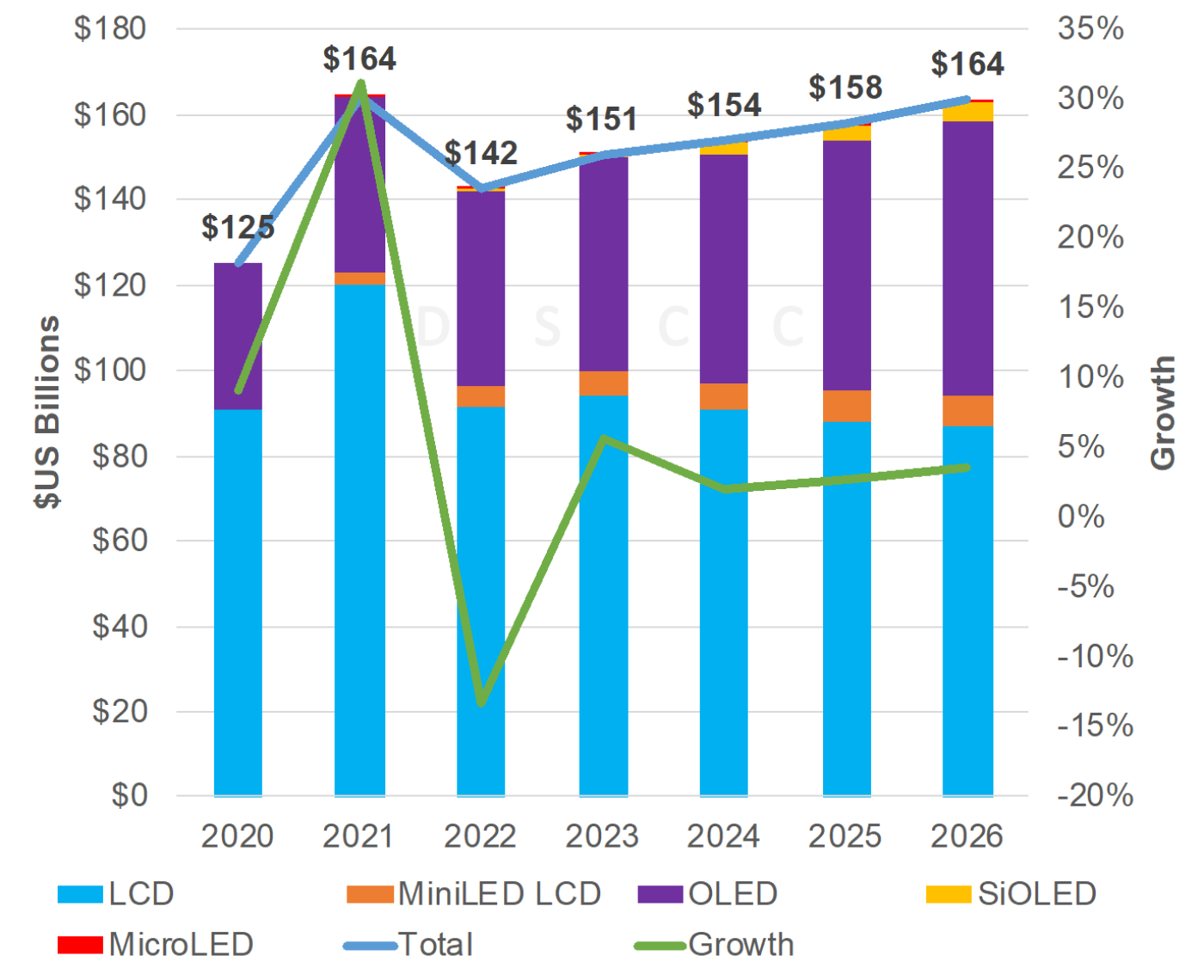

COVID-19 pulled in significant demand while at the same time supply was constrained leading to much higher prices and unusually high growth. Display revenues rose 31% Y/Y in 2021 to a record $164B. This was achieved due to strong demand from work from home (WFH) and learn from home (LFH) with notebooks rising around 100M units from 2019 to 2021. Utilization trended upward in 2020 and 1H’21, as demand growth outpaced supply growth. LCD equipment spending was down 26% in 2020, which led to the slower supply growth. Utilization would have been even higher without component shortages. With supply/demand tight and driver IC shortages persisting, panel manufacturers and brands focused on higher margin products, further boosting display margins. Display stocks outperformed many other indexes until April 2021 when panel prices began to level off.

In 2020 and 2021, there was high double-digit revenue growth in five different segments – monitors, notebook PCs, smart watches, tablets and TVs. The IT panel revenue share surged from 20% in 2010 to 29% in 2021 on strong unit growth, price increases and MiniLED adoption. TVs rose from a 25% to a 28% share on price increases and area growth. Mobile phones fell from 38% to 30% but remained the largest segment. The average display diagonal rose by 7% from 2019 to 2021 to 11.0” with monitors up 5% to 25” and TV diagonals rising 8% to 47”. TVs remained the dominant segment on an area basis with a 69% share in 2021.

The surge in LCD prices enabled LCDs to outgrow OLEDs in 2021 with a 35% to 20% advantage with LCDs boosting their share to 75% of the display market. MiniLEDs rose to a 2% share in 2021.

BOE became the top panel supplier in revenues with a 19.1% share on 73% growth. SDC fell to #2 but LGD significantly narrowed the gap. SDC remained dominant in OLEDs with a 59% share, down from 65%, with LGD at #2 at 23%. Chinese suppliers still account for less than 20% share despite massive capex. In LCDs, there was double-digit growth for the top eight suppliers. BOE’s advantage rose from two points to nine points on its capacity expansions and well-timed CEC Panda acquisition. LG Display remained #2 followed by AUO, Innolux and China Star. Operating margins, stock prices by supplier and our panel supplier stock index were also shown.

Young notes that while most industries, and by extension consumers and end-users, are seeing price increases for goods rise on inflation, supply disruptions and shortages, display prices have been, and are still, falling this year due to a lot of new LCD capacity coming online, as well as slower than expected demand growth.

Demand, he notes, is not responding to lower panel prices for numerous reasons, such as:

- Higher inflation from COVID-related fiscal and monetary stimulus;

- Russia-Ukraine war impacting demand and sanctions against Russia worsening inflation on higher energy and food prices;

- Extended COVID-19 shutdowns in China – impacting supply chains and demand and potentially inflation;

- Saturation in consumer IT and TV purchases;

- Less discretionary spending due to higher oil prices, transportation costs, food prices, housing prices, costs of capital, etc.;

- Governments raising rates and trying to slow down demand;

- Consumer spend shifting from hardware to services.

At the same time, display suppliers are experiencing cost increases due to:

- Rising energy prices impacting transportation/shipping costs;

- Certain material prices being impacted by rising oil prices – PI, CPI, PET, etc.;

- Neon gas used for ELA and LLO, ~30% of production in Ukraine, especially Mariupol (Ingas) which has been hit hard.

Demand is being impacted around the world this year with global GDP being cut from 4.9% to 3.6%, US GDP growth cut from 5.2% to 3.7%, EU cut from 4.3% to 2.8%, Japan cut from 3.2% to 2.4% and China cut from 4.8% to 4.4% per the IMF. As the IMF said, there is unusually higher uncertainty surrounding forecasts this year with downside risks dominating.

Last year, we were far more optimistic for the LCD industry in 2022 and beyond, because panel manufacturers had restrained themselves with their capex plans. However, over the past year, we have seen numerous new fab and capacity expansion announcements. As a result, LCD supply growth is now significantly higher than previously expected, 16% higher for 2022 vs. our Q1’20 forecast and 22% higher for 2025 vs. our Q1’20 forecast. Furthermore, much of this investment is happening in IT markets as panel suppliers believe the boom in IT markets will continue. OLED suppliers are also targeting the IT market with their new investments. However, the IT market peaked in 2021. Thus, we will see much of this new capacity reallocated to automotive, which is growing and we will likely see growing price competition in the IT space leading to higher penetration for more advanced IT panels – OLED, MiniLED, IGZO backplanes, etc.

You can get at the full summary of Young’s keynote by registering with DSCC …

Leave a comment