Research: 800,000+ Digital Signage Displays Shipped Q1 2017

August 21, 2017 by Dave Haynes

LOTS of interesting stuff in the new IHS Markit Digital Signage & Professional Displays Market Analysis, this one for Q2 2017.

Here’s the top-line stuff in the executive summary:

For the first quarter of 2017 (Q1 2017), public display monitor shipments increased 2.6%, with shipments reaching over 804,000 units.

Public display TV shipments recovered from the previous quarter’s drop with an increase of 13.6% based on the lift in shipments by LGE and Sharp of 24.4% and 16% quarter-on-quarter (QoQ), respectively. Samsung’s public display TV shipments continue to decline this quarter as RMD and RHE series are discontinued, with an additional 51.7% QoQ dip in its public display TV shipments.

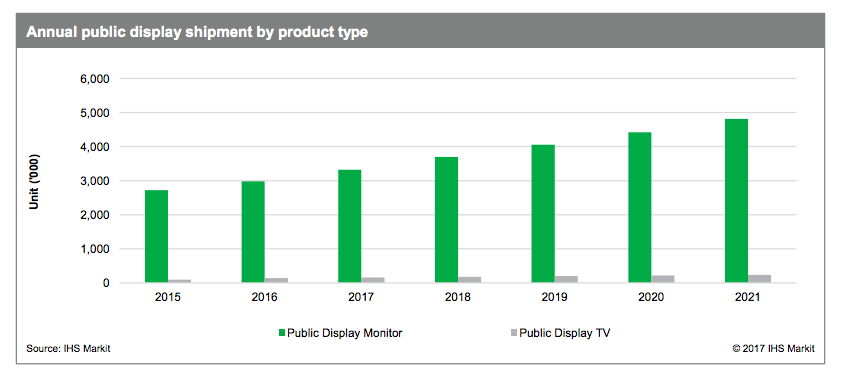

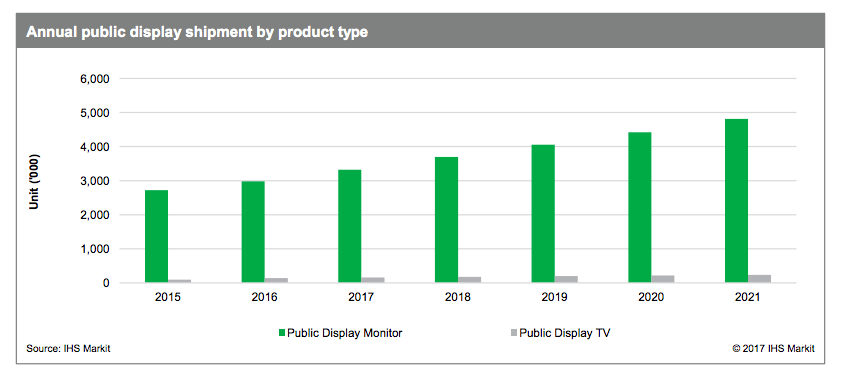

IHS Markit expects public display monitor shipments will exceed 4.8 million units by 2021, while public display TVs will surpass 240,000 units by 2021.

For Q1 2017, the most popular sizes continue to be 43-inch, 49-inch, and 55-inch sizes for public display monitor shipments, increasing 19.2%, 31.8%, and 10.7%, respectively, over the previous quarter. Shipments of 85-inch public display monitor shipments showed significant growth this quarter, more than doubling its share relative to the previous quarter by 152.9%, reaching just over 2,600 units.

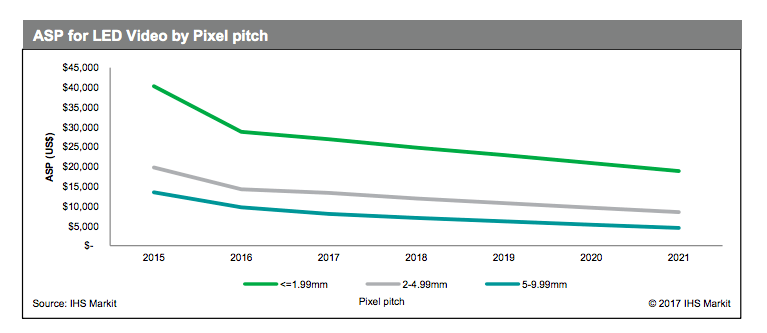

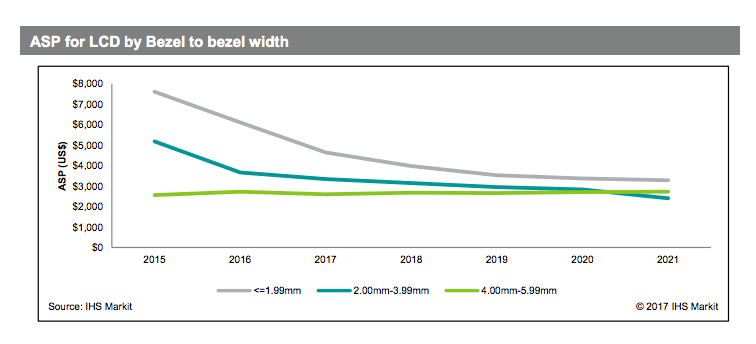

There’s a lot in the report, but what was different and interesting to me was a look at narrow bezel LCD versus fine pitch LED, and how prices are dropping for both types of displays.

- The ASP (Asking Street Price) for LED video displays are naturally higher than LCD, however, bezel-less displays is a chasm LCD technology cannot cross. When comparing the ASPs for both technologies, it is essential to look at larger format super narrow bezel width LCD displays and finer pixel pitch LED video for a fair comparison.

- ASPs for narrow bezel products continue their drop, bezel width less than 1.99 mm decreased 20% YoY in 2016, and is forecast to drop 46% by 2021. Similarly, for bezel width between 2 mm and 3.99 mm, ASPs has decreased 29% YoY in 2016; they are forecast to reduce 34% by 2021.

- LCD narrow bezel (less than 1.99mm) products currently are available in a limited number of screen sizes: 49–55 inches. The latter currently is generating most of the revenues, while 49 inches is forecast to surpass 55 inches in revenue and lead growth in 2019.

- Narrow bezels revenue is forecast to be multiplied by 10 by 2021, reaching over $773,000.

- ASPs for LED fine pixel pitch products (less than 1.99mm) show a similar level of decline, -29% YoY; they are forecast to reduce by 35% by 2021.

The IHS quarterly report costs real money, but Digital Signage Federation members get it free as part of their membership perks.

Leave a comment