Global Ad Spend Up, Mobile Biggest Growth Driver: ZenithOptimedia Report

April 7, 2014 by Dave Haynes

The giant ad agency holding group ZenithOptimedia has issued a report this morning predicting that global ad spend will grow by 5.5% in 2014, reaching US$537B by the end of this year.

That number is up from the December 2013 version of its quarterly forecast – owing primarily to what’s seen as stronger growth in the Americas and Asia Pacific.

Advertising will continue to strengthen over the next three years, with global advertising spend growth forecast to rise from 3.9% in 2013 to 5.5% in 2014. Growth is then set to increase to 5.8% in 2015 and 6.1% in 2016. This growth will be driven by improvement in the global economy, the spread of programmatic buying, and the rapid rise of mobile advertising.

According to ZenithOptimedia’s new Advertising Expenditure Forecasts, global adspend will be boosted this year by the three ‘semi-quadrennial’ events – the Winter Olympics, the football World Cup, and the mid-term elections in the US – which will benefit television in particular. Advertisers are also gaining in confidence as growth returns to the Eurozone, which now looks more stable and less likely to deliver more negative shocks to the world economy. In general, advertisers are in a strong position to invest in expansion, with large reserves of cash and high profitability. In view of this, we expect growth to increase in each of the three years we forecast.

The report breaks down spend by region, and also by category.

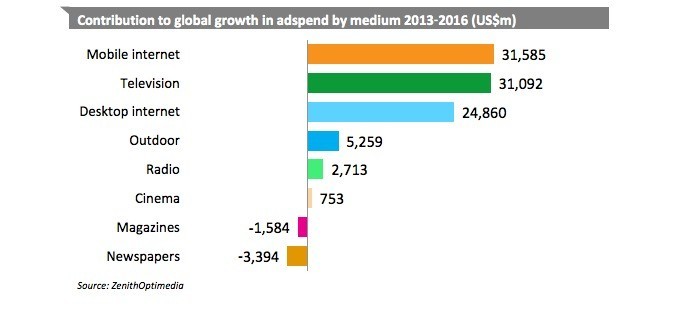

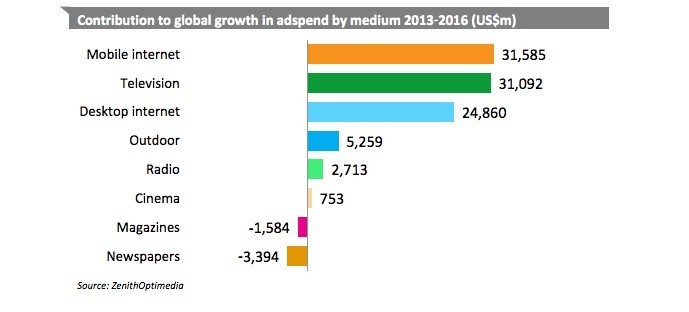

Mobile is now the main driver of global adspend growth. We forecast mobile to contribute 35% of all the extra adspend between 2013 and 2016. Television is the second largest contributor (accounting for 34% of new ad expenditure), followed by desktop internet (27%).

Television is still by some distance the dominant advertising medium, attracting 40% of spend in 2013, nearly twice that taken by desktop and mobile together (21%). Television offers unparalleled capacity to build reach, and establish brand awareness and associations. We forecast television adspend to grow 5.2% in 2014, up from 4.4% in 2013, as it gains the most of the benefits of the Winter Olympics, the football World Cup and the mid?term US elections. We then expect growth to fall back to 4.4% in 2015 before rising to 5.1% in the quadrennial year of 2016 (with the Summer Olympics, European football and US presidential election).

Despite this healthy growth, television’s share of global adspend is likely to fall back slightly over the next few years as desktop and mobile internet grow much faster. Television’s market share has grown steadily over the last three and a half decades, from 30.7% of spend in 1980 to 40.1% in 2013. We think it has now peaked, however, and forecast it to fall back marginally to 39.2% in 2016.

Digital OOH or place-based or whatever you want to call it is not a big enough medium to get its own call-out in this report. Depending a little on how a network goes to market and what it deliver, you might see it fall into the TV bucket, or OOH or even online video.

The report suggests internet is still the fastest growing medium by some distance. It grew 16.2% in 2013, and we forecast an average of 16% annual growth for 2014 to 2016.

Display is the fastest?growing sub?category, with 21% annual growth, thanks partly to the rapid rise of social media advertising, which is growing at 29% a year. Measurement agencies are investing in research that should measure consumers’ exposure to traditional display ads more accurately, and track their exposure to video ads across desktop computers, tablets and television screens. Some broadcasters are starting to trade packages that include both online video and television spots; online video is also starting to be sold by programmatic buying, providing advertisers with more control and better value. We forecast online video to grow at 23% a year for the rest of our forecast period.

We expect paid search to grow at an average rate of 13% a year to 2016, driven by continued innovation from the search engines, including the display of richer product information and images within ads, better localisation of search results, and mobile ad enhancements like click?to?call and geo?targeting.

Online classified has been subdued since the downturn in 2009; after the initial shift from print to digital, classified publishers have had to compete with new paid?for and free alternatives for matching buyers and sellers. We forecast average annual growth of just 6% for the rest of our forecast period.

Mobile advertising (by which we mean all internet ads delivered to smartphones and tablets, whether display, classified or search, and including in?app ads) has now truly taken off and is growing six times faster than desktop internet. We forecast mobile advertising to grow by an average of 50% a year between 2013 and 2016, driven by the rapid adoption of smartphones and tablets. By contrast we forecast desktop internet advertising to grow at an average of 8% a year.

We estimate global expenditure on mobile advertising at US$13.4bn in 2013, representing 12.9% of internet expenditure and 2.7% of total advertising expenditure (this total excludes a few markets where we don’t have a breakdown by medium). By 2016 we forecast this total to rise to US$45.0bn, which will be 28.0% of internet expenditure and 7.6% of all expenditure. This means mobile will leapfrog radio, magazines and outdoor to become the world’s fourth?largest medium

by the end of our forecast period.

Since it began in the mid?1990s, internet advertising has principally risen at the expense of print. Between 2003 and 2013 the internet’s share of global advertising rose by 17 percentage points, while newspapers’ share fell 14 points and magazines’ share fell by 5 points. We predict internet advertising will increase its share of the ad market from 20.7% in 2013 to 27.1% in 2016, while newspapers and magazines will continue to shrink at an average of 1%?2% a year. Internet advertising overtook newspaper advertising for the first time in 2013, and we forecast it to exceed the combined total of newspaper and magazine advertising in 2015.

Note that our figures for newspapers and magazines include only advertising in printed editions of these publications, not on their websites, or in tablet editions or mobile apps, all of which are picked up in our internet category.

The report is a free download here.

Leave a comment